Revenue-Based Financing: How It Works and When To Use It

Revenue-Based Financing: Key Takeaways

- With revenue-based financing (RBF), you receive capital and repay it as a share of your monthly revenue

- The total repayment amount is agreed upfront, while monthly payments vary based on business performance

- It’s generally a better fit for businesses generating consistent revenue month after month

- Compared to traditional loans, it gives you quicker access to capital, with repayments that adjust as your revenue changes

- Revenue-based financing can be used for inventory, marketing, unexpected expenses, or short-term growth opportunities

The revenue-based financing market is growing rapidly and is projected to reach nearly $110 billion by 2030, according to research firm Research and Markets.

More businesses are clearly exploring alternatives to rigid loan structures, especially when cash flow doesn’t follow a predictable pattern.

In this guide, we’ll cover:

- How revenue-based financing works

- What the typical cost structure is

- How it compares to traditional loans

- The main advantages and drawbacks

- When you may want to consider revenue-based financing for your business

How Revenue-Based Financing Works

Compared to traditional loans, the process tends to be more streamlined, with fewer steps and faster turnaround times.

Application & Evaluation

Instead of focusing heavily on your credit score, lenders look at how your business actually performs: your revenue, consistency, and cash flow trends.

From there, you’re offered a lump sum, which is repaid as a fixed percentage of your monthly revenue.

Repayment Agreement

Instead of interest, you agree to repay a flat payback amount that is based on your industry and business performance. In some cases, that might mean repaying as much as double the original funding amount.

Revenue-Based Payments

Repayments come directly from a percentage of your monthly revenue, typically ranging between 5% and 20%, which allows payments to fluctuate with sales.

Repayment Completion

Revenue-based financing does not have a fixed repayment term because repayment depends on how quickly your business generates revenue.

RBF: Repayment Terms and Cost Structure

Rather than locking you into fixed monthly payments, this structure adjusts based on your cash flow. When you make less money, your payments decrease.

Here’s a simple way to look at it:

A business receives $100,000 in funding with a repayment multiple of 1.3x. This means the total repayment amount is $130,000. The lender also sets a repayment rate of 10% of monthly revenue.

- If the business generates $50,000 in a month, the payment is $5,000.

- If revenue drops to $30,000, the payment decreases to $3,000.

Payments continue to adjust based on revenue until the full $130,000 is repaid.

Strong revenue shortens the repayment timeline, while slower periods stretch it out, without changing the total owed.

No Fixed Timeline

Since payments fluctuate, the timeline isn’t fixed. Strong months shorten the term, while slower periods extend it.

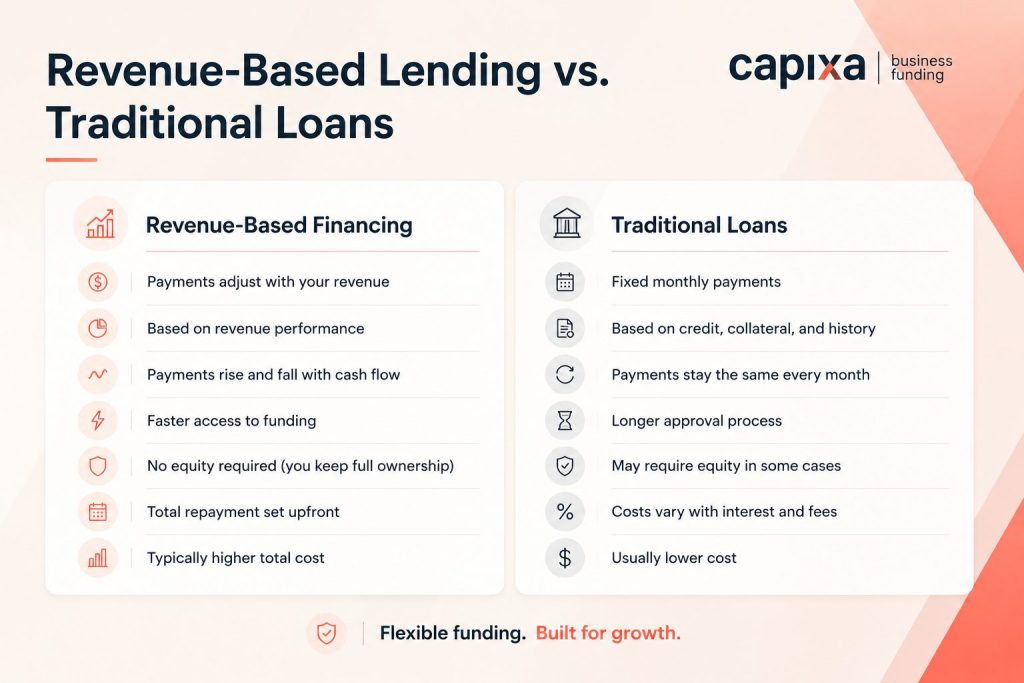

Revenue-Based Lending vs. Traditional Loans

To determine which option is best for your business, you must know the difference between the two.

Payment Structure

A key difference comes down to repayment. With revenue-based financing, payments shift with your sales.

Traditional loans don’t: Payments stay fixed regardless of performance.

Approval Criteria

With RBF, approval is tied closely to how your business is performing.

Traditional lenders, on the other hand, still lean heavily on credit scores, collateral, and financial history.

Flexibility

With revenue-based financing, payments may be reduced if your revenue decreases.

With traditional loans, the repayment structure remains the same month after month.

Approval Speed

Funding through revenue-based financing is faster to secure, which can matter in time-sensitive situations.

Traditional loans involve a longer underwriting process with more documentation and requirements.

Ownership

Revenue-based financing does not require you to exchange funding for equity, meaning, you retain full ownership of your business.

In contrast, with some traditional financing alternatives, such as equity financing, you must give up a portion of ownership in exchange for capital.

Cost Transparency

One advantage of revenue-based financing is that the total repayment amount is defined upfront.

Traditional loans involve interest rates, compounding, and additional fees, which means you must perform complex calculations to discover the total cost.

Cost

Revenue-based financing typically has a higher total cost compared to traditional bank loans because funders take more risk by providing capital in exchange for future revenue not yet received.

Repayment depends on the business continuing to generate revenue, which increases the overall risk exposure for the funding provider.

Traditional loans, especially from banks, typically offer lower borrowing costs, as they are priced using interest rates.

When Revenue-Based Financing Makes Sense

This type of funding tends to make the most sense for businesses with steady, predictable cash flow.

That typically includes handling regular transactions, running subscription models, or dealing with frequent customer turnover.

These businesses can use RBF for:

- Purchasing inventory ahead of a peak sales period

- Covering unexpected expenses for equipment repairs

- Taking advantage of a limited-time discounted bulk order

- Funding an urgent marketing campaign

- Managing short-term cash flow gaps

- Securing a new contract that requires upfront costs

- Business expansion or growth, adding employees, or opening a new location

Pros and Cons of Revenue Based Financing

While this model offers flexibility, it is important to weigh its benefits against its potential drawbacks.

Pros

- Payments adjust with your revenue, which can ease pressure during slower months

- Fast access to capital, particularly when time matters

- You retain full ownership of your business

- You can use the capital for inventory, hiring, marketing, or expansion, depending on your needs

- You can apply for funding even with a weak credit profile

Cons

- In many cases, the total repayment ends up higher than what you’d pay with traditional financing

- If revenue drops significantly, it can take longer than expected to fully repay the amount

- Giving up a percentage of revenue can strain businesses with tight margins

- Businesses with unpredictable revenue may find it harder to qualify

Support Your Business Growth With Revenue-Based Financing From Capixa

Capixa structures revenue-based financing around how your business earns and grows rather than forcing you into fixed repayment terms.

Whether you work in construction, restaurants, healthcare, real estate, and retail, we provide capital solutions that align with your operations, cash flow, and growth plans.

If revenue-based financing is not the right fit, we offer alternative solutions such as small business loans, business term loans, and business lines of credit.

The process is simple: Submit a short application, connect with a dedicated account manager to review your options, receive a decision within hours, and access funding quickly once approved.

Revenue-Based Financing: FAQs

What is revenue-based financing?

It’s a type of business funding in which repayment is based on your revenue instead of fixed monthly payments.

Is revenue-based financing the same as a loan?

Unlike traditional loans, revenue-based financing is structured as the purchase of future receivables for a fixed sum rather than borrowed money. That’s why, the repayment structure and overall terms work differently from traditional business loans.

How quickly can I get RBF funding?

In many cases, funding can be approved faster than traditional bank loans. In some cases, we’ve approved revenue-based financing in less than an hour after receiving a completed application and three months’ worth of bank statements.

What happens if my revenue drops?

Because payments are tied to your revenue, businesses experiencing a drop, can request a reconciliation by providing updated bank statements. If approved, payments may be adjusted based on the agreed prepayment structure.

Can I repay early?

Yes, but keep in mind that the total repayment amount is usually fixed, so early repayment may not reduce the overall cost. However, some agreements may include early repayment discounts depending on the financing structure and business profile.

![What Is a Small Business Loan [How it Works + Types of Loans]](https://capixa.com/wp-content/uploads/2024/09/what-is-a-small-business-loan-hero-image.jpg)